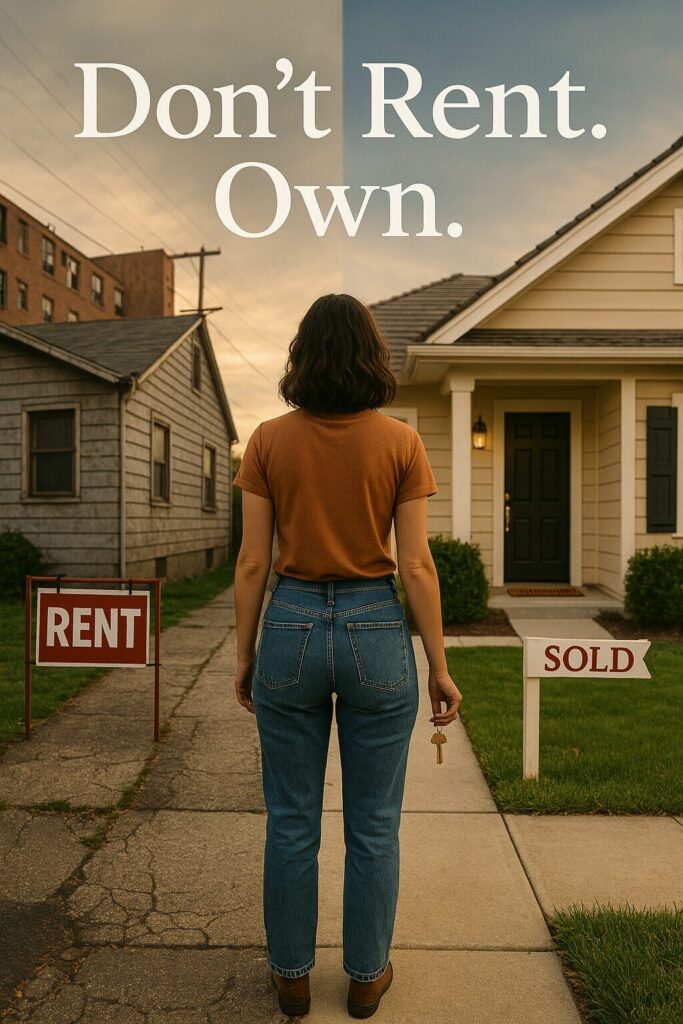

Let’s be real—buying a home feels overwhelming. Between confusing loan options, conflicting advice online, and that nagging fear of rejection… it’s no wonder many people stay stuck renting year after year.

But here’s the truth no one talks about enough: residential real estate financing doesn’t have to be a mystery or a trap. In fact, when you work with the right lender or advisor, it becomes your most powerful tool to build real wealth.

So whether you’re tired of paying your landlord’s mortgage or ready to upgrade your living situation, let’s break down what actually matters when it comes to getting financing—and getting into your home.

1. You Don’t Need a Perfect Credit Score (Seriously)

A lot of people assume you need a 750+ credit score to qualify. False. While better credit helps you get the best rates, many lenders approve buyers in the mid-600s with strong income and a reasonable down payment.

Pro Tip: Pull your credit report early and fix any errors. A quick 20-point bump could mean thousands saved in interest.

2. There’s More Than Just the 30-Year Fixed

That’s the classic option—but not the only one. Depending on your goals, there may be better fits:

- Adjustable Rate Mortgages (ARMs) for short-term stays

- 15-year loans to pay off faster

- FHA & VA loans with low down payments

The best loan isn’t always the most popular—it’s the one that fits your life.

3. Down Payments Are Flexible

You don’t need 20%. Repeat that out loud. There are solid loan options that let you get in with as little as 3% down. And some areas even offer down payment assistance or grants—especially for first-time buyers.

Bottom line? The sooner you stop chasing perfection and start exploring options, the closer you get to keys in hand.

4. Lenders Are Partners—If You Choose the Right One

The right lender isn’t just there to approve or deny you—they’re your guide. Ask questions. Expect education. And if you’re working with someone who talks at you instead of with you? Move on.

You deserve a loan officer who sees the big picture and wants to build a relationship, not just close a deal.

5. Timing the Market Is a Trap—Focus on Timing Your Life

Yes, rates go up and down. But trying to “time the market” perfectly has kept more people renting than it’s helped. If you’re financially ready, stable in your job, and planning to stay for a few years—you’re ready to buy.

Marry the house, date the rate. You can always refinance later.

🎁 Final Thought: Your Dream Home Isn’t as Far as You Think

Financing doesn’t have to be a brick wall—it can be a bridge. The key is asking the right questions, connecting with the right people, and realizing that waiting forever won’t make the process easier.

Let’s make your next move smarter, not harder.

#HomeBuyingJourney #SmartHomeFinancing #MortgageMadeSimple #FromRenterToOwner #RealEstateTips

Call us 832-539-7557 or email us info@fenixsolutions.io

Follow for more: www.fenixsolutions.io/blog